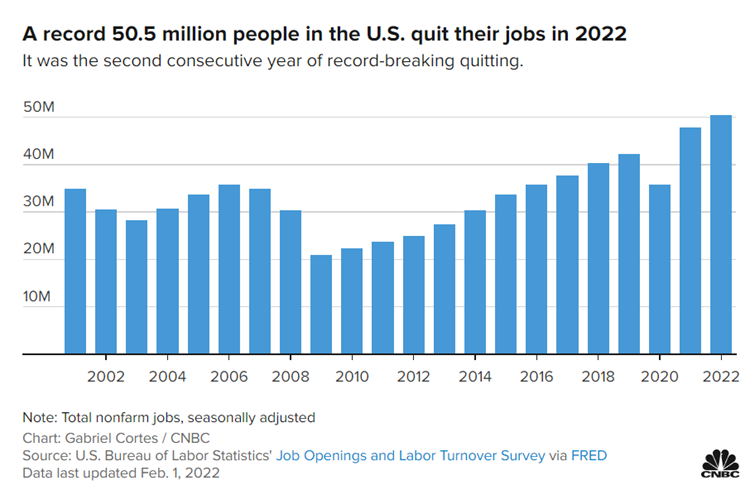

The pace of change in insurance continues to accelerate and keeping up remains a challenge for insurers. In 2022, the auto insurance industry saw its highest combined ratio in the last two decades, and in property, natural catastrophe losses topped $270 Billion. Additionally, roughly 50.5 million people quit their jobs in the US, which is more than any other year including the “Great Resignation” of 2021.

See Also: Download our survey of over 2000 consumers to learn about trends in consumer expectations

Today’s risk profile is much different than it was 10, 20, or 30 years ago. Since the year 2000, over half the Fortune 500 Companies no longer exist. In this short read, I’d like to walk through 3 high level trends, and why insurers need to rethink their homegrown, legacy core systems in order to navigate these trends, or face dire consequences.

Trend 1: Workforce Changes

First, the workforce is changing. This trend is impacting insurers at an alarming rate – not only are they losing tribal knowledge acquired over years of experience specific to their company, but they are also competing to attract a new generation of talent. As of 2021, the population in the US of Millennials and Gen Z when combined reached a total of ~141 million, meaning roughly half of the US is under 40 years old!

According to a Career Builder survey, Millennials and Gen Z, on average spend less than 3 years in a role. Compared to the insurance industry where many have been at their organization for decades and in some cases their entire career.

This is a clear difference in mindset between the generations.

How does a changing workforce impact insurance systems?

The loss of talent paired with the need to attract new, qualified talent is a significant challenge. And, for carriers that are leveraging legacy systems this loss makes it even more difficult.

It is almost impossible to replace nuance systems knowledge gained over years, find someone with the mainframe technical skills (e.g. Cobol programming), and compete with competitive wages and hybrid / remote pressures. Not to mention, the less than 3-year average role tenure, which ultimately impacts training and hiring costs.

Candidly, the pool of candidates to hire from when operating on legacy homegrown systems is slim to none. This changing workface makes goals like developing new products, improving payments and billing, or straight through processing of claims, extremely challenging.

Trend 2: A Changing Customer Base

Similar to the workforce, your customer base is also changing. This trend impacts not only the target buyers of insurance, but the types of insurance products in demand.

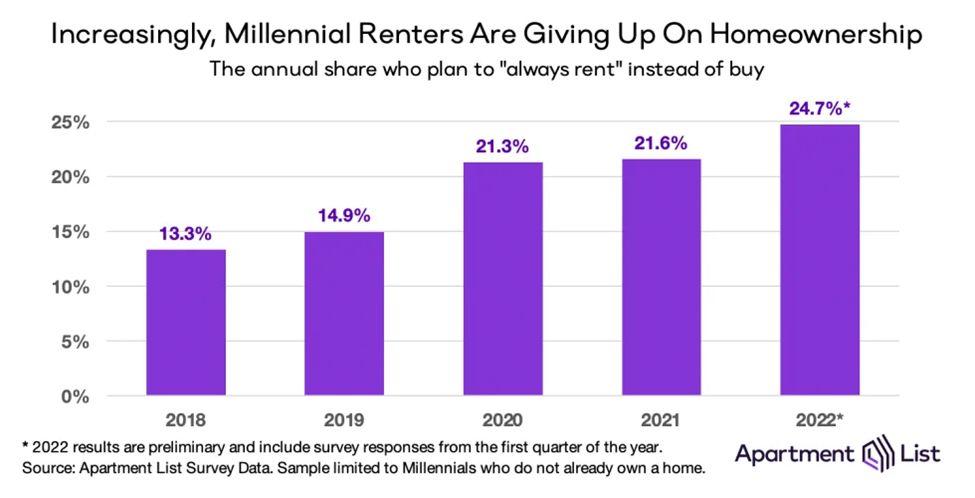

For example, in the past 3 years, Gen Z’s estimated disposable income has doubled to roughly $360 billion. Interestingly enough, side gigs (or the hustle economy) accounts for almost $40 billion of their income. Also interesting is that just shy of 25% of millennials said they would rent forever, which is almost double the sentiment in 2018.

Trends like these are impacting product demand. More entrepreneurs and gig economy workers – doing everything from ridesharing to food delivery to construction – requires more specialized products for contractors, as well as small business insurance and workers’ comp.

Less ownership impacts home and rental insurance. As younger generations continue to rent, there will be a natural shift in demand for insurance products. Furthermore, more work from home could also mean more usage-based auto insurance leveraging telematics.

How does a changing customer base impact insurance core systems?

Meeting evolving customer demands requires more personalized coverages, and policy administration systems that enable insurers to accelerate speed to market.

But aside from providing the right coverages, insurers also need to focus on their customer’s experience. Consumers expect the speed and ease of Uber; the customer service of Amazon; the variety of AirBnB. These are the companies’ carriers will need to compete with as they think about the UI and CX their customers, agents, and employees expect.

In very rare occasions are carriers able to deliver these experiences with homegrown systems, nor should they. With limited resources, a modern core system can free up IT to focus on supporting product development and UX, not routine maintenance for keeping the lights on.

Trend 3: Legacy Mindset

The last trend is something that I like to call “Legacy Mindset,” and this might be one of the biggest hurdles of all. Unfortunately, this idea that “we’ve been in business for over a hundred years,” is still prevalent in many organizations and is holding them back from the advancements they will need in order to be around for the next one hundred years.

The changing global environment with geopolitical risks, cyber security concerns, supply chain impacts, and catastrophic events is putting significant pressure on expense ratios, profitability, and premiums. The insurance company from 100 years ago isn’t equipped to deal with today’s risk. Instead of thinking about how to address these challenges, the legacy mindset prevents insurers from taking action, as they feel the status quo has gotten them this far and will continue to do so. However, this isn’t the case.

How does this mindset impact insurance systems?

Here are a few examples of how the risk profile has changed and why leaders need to think about things differently:

- Cyber Risk – according to Barracuda, in 2022 small organizations, of less than 100 employees, saw 350% more social engineering attacks than large organizations. While in 2021, Accenture reports an increase of 31% in the average amount of cyber-attacks across companies when compared to 2020.

- Given the increase in cyber risk, organizations need to consider if they can better manage cyber security with their limited budgets and resources or would a SaaS partner actually be more secure.

- Claims – labor and material costs have increased, while inflation was as high as 9.1% in June of 2022.

- This is putting increased pressure on organizations to either price more accurately or reduce other costs. Leveraging a SaaS partner can actually be less expensive than maintaining legacy systems and allow for quicker rate changes.

The fact is companies need to invest in new SaaS systems that can help with the new normal, rather than re-create the technical debt many have been stuck in for decades.

Older organizations are competing with the new kids on the block: Insurtechs, digital first organizations, embedded insurance, and direct-to-consumer options will continue to change and shape the insurance industry for years to come.

Carriers with legacy systems often struggle with operational efficiency, increasing speed to market, leveraging best in class technology, digital customer service, and personalizing experiences. Forward-thinking, digital-first organizations embrace technology that provides the flexibility to execute on new initiatives – whether that be partnering with brands to offer embedded insurance, or simply providing a new direct-to-consumer option.

“Hybrid” Insurance Solutions are the Answer

My personal belief is that trends like these will continue to impact the insurance industry. So, what needs to be done?

The good news is that these challenges are not insurmountable. In fact, when addressed properly, they can actually lead to a competitive differentiator and higher premiums.

Insurers need the right combination of technology partner(s), executive buy-in, external resources to supplement your teams who are focused on running the business – and ultimately the willingness to change.

While digital transformation can be a daunting task, you are not alone. There are a variety of SaaS technology providers and systems integrators that can help with your individual journey.

Let me leave you with this — change isn’t as simple as “Build vs Buy;” there is a best of both worlds option that provide a “hybrid” approach.

“Hybrid solutions”, like Duck Creek OnDemand provide an “off-the-shelf” platform you can buy with rich functionality and content across the insurance lifecycle, but at the same time are highly flexible with low-code configuration tools, pre-built integrations to the broader ecosystem, and are continuously updated with new features. These capabilities allow you to still be able to build the best possible experiences for your producers, customers, and employees.

Are you interested in chatting more about any of these trends or re-thinking your homegrown systems? Feel free to reach me at r.rodriguez-wiggins@duckcreek.com to discuss more.